Why Identical Pine Script Strategies Behave Differently Across Assets | Cross-Market Strategy Analysis

Author : Ranga Technologies

Publish Date : 5 / 6 / 2026 • 1 mins read

Last Updated : 5 / 6 / 2026

When “The Same Strategy” Produces Completely Different Results

A trader builds a profitable TradingView strategy using BTCUSD data. Backtests look consistent. Drawdowns are controlled. Equity grows steadily. The same script is then applied to:

- EURUSD

- NASDAQ

- Gold

Suddenly:

- Profitability collapses

- Drawdowns increase

- Trade frequency changes

- Win rate drops

- Nothing in the code changed.

So why did the performance change dramatically?

This case study explains the hidden structural differences between assets, how they silently reshape strategy outcomes, and how AI-assisted Pine Script engineering helps stabilize performance.

The Invisible Forces Driving Asset-Specific Performance

Many Pine Script strategies assume markets behave similarly. In reality, each asset class operates under different structural conditions:

- Volatility regimes differ

- Liquidity profiles vary

- Session behavior changes

- Trend persistence varies

- Spread and noise characteristics differ

Even if the strategy logic is identical, the environment where the logic executes is not.

Real Testing Scenario

A simple EMA crossover strategy with ATR-based stop loss was tested across multiple assets using the same:

- Timeframe

- Risk model

- Parameters

- Entry/exit rules

- Only the underlying asset changed.

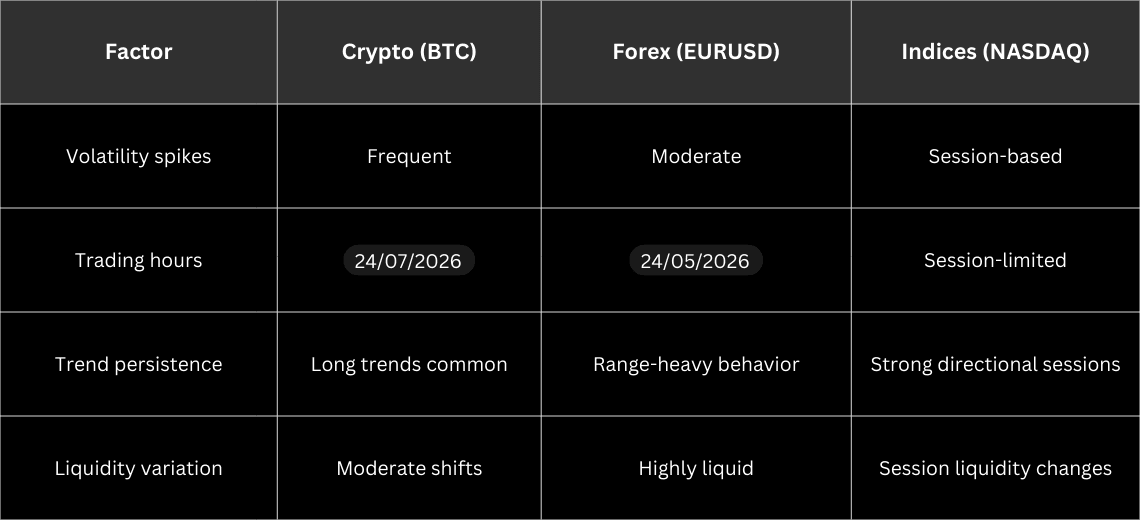

Asset Structure Differences

Because strategies react to price movement characteristics, identical logic reacts differently in each environment.

What Actually Breaks Strategy Consistency

When assets change, the following silent mismatches appear:

- ATR-based stops become too tight or too wide

- Entry signals trigger more often due to volatility structure

- Trend filters lose effectiveness in ranging markets

- Exit timing becomes misaligned with asset behavior

- Position holding duration shifts dramatically

The script remains identical, but the statistical context changes.

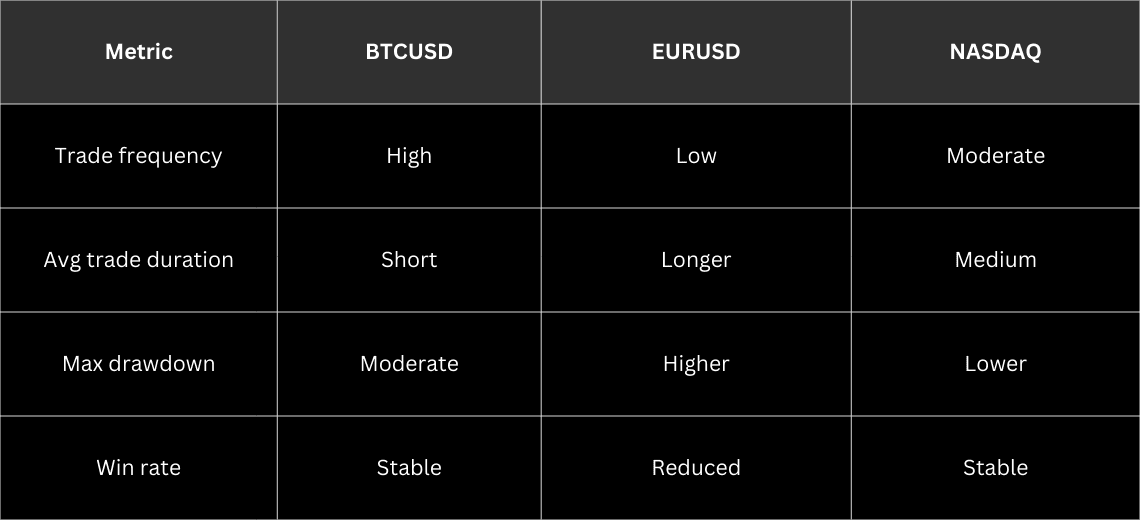

Performance Drift Example

This explains why many traders believe:

“The strategy stopped working,” when in reality the asset environment changed.

Engineering Asset-Adaptive Risk Logic

To stabilize multi-asset performance, strategies must adapt dynamically using:

- Volatility normalization (ATR regime detection)

- Session-aware filters

- Trend strength thresholds

- Liquidity-aware execution logic

- Adaptive stop-loss multipliers

Instead of static parameter values, the strategy reacts to current asset conditions.

How PineGen AI Helped Resolve the Issue

During internal PineGen AI testing workflows, the same strategy was restructured to include:

- Volatility-adaptive risk blocks

- Asset-sensitive entry filters

- Parameter normalization across markets

- Strategy tester logic validation

After adjustment:

- Cross-asset performance variance reduced

- Drawdown distribution stabilized

- Trade quality improved without curve fitting

Rather than forcing parameter optimization for each asset manually, AI-assisted logic structuring reduced repeated tuning cycles.

What Traders Often Misinterpret

Many traders assume:

- A strategy is universally profitable

- Backtest success equals cross-market robustness

- Parameter optimization alone solves the issue

In reality, market structure alignment matters more than parameter tuning.

Key Takeaways

- Identical Pine Script strategies behave differently because assets operate under different volatility, liquidity, and session dynamics.

- Static stop-loss and entry parameters rarely scale across markets.

- Asset-adaptive logic dramatically improves consistency.

- AI-assisted Pine Script engineering reduces repeated re-optimization cycles and helps structure cross-asset compatible strategies.