Why Liquidity Feels Thinner in the U.S. Markets Despite High Volume

Author : Ranga Technologies

Publish Date : 4 / 15 / 2026 • 2 mins read

Last Updated : 4 / 15 / 2026

If trading volume is at record highs… Why does the price still move like there’s no liquidity?

Why do trades slip, spreads widen, and levels break faster than expected?

This case study explores a growing contradiction in U.S. markets: high trading volume but declining effective liquidity. It explains how modern market structure, driven by algorithmic trading, fragmented exchanges, and order execution strategies, creates an environment where price moves faster, execution becomes harder, and traditional strategies lose reliability.

1. Problem Statement

Traders today are facing a paradox:

-

Volume is high

-

Markets are active

-

Yet execution feels worse

Common issues:

-

slippage during entries and exits

-

sudden price jumps

-

inconsistent fills

-

stop-losses triggered unexpectedly

In highly traded indices like the S&P 500, this issue is becoming more visible, especially during volatile sessions.

2. Why Liquidity Matters

Liquidity is not just about how much is traded, it’s about how easily trades can be executed without moving price.

Strong liquidity means:

-

tight bid-ask spreads

-

deep order books

-

stable price movement

Weak liquidity means:

-

wider spreads

-

thin order books

-

sharp price changes

So even if volume is high, liquidity can still be functionally weak.

3. What Changed in the U.S. Markets

Modern market structure has evolved significantly.

Key changes include:

3.1 Algorithmic Trading Dominance

A large portion of trades are now executed by algorithms.

These systems:

-

split orders into smaller pieces

-

react to micro price movements

-

remove liquidity quickly

3.2 Fragmented Market Structure

Orders are spread across multiple venues:

-

exchanges

-

dark pools

-

internalized broker systems

This reduces visible liquidity in any single order book.

3.3 Rise of High-Frequency Trading (HFT)

HFT firms:

-

provide liquidity

-

but also remove it instantly

They adjust positions in milliseconds, making liquidity: Present, but unstable

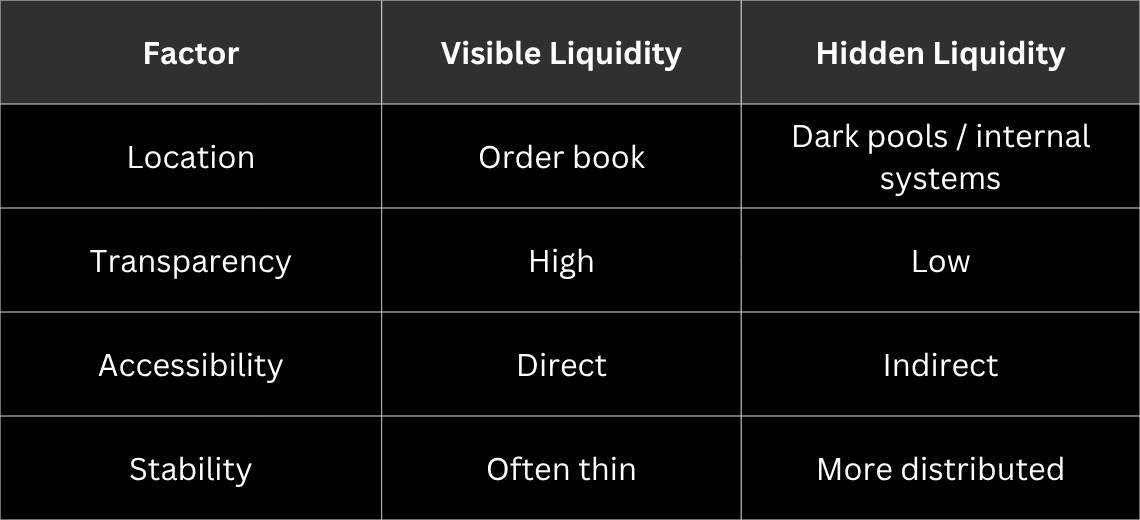

Hidden vs Visible Liquidity

One of the biggest reasons liquidity feels thinner is the gap between:

Displayed liquidity (what you see)

Actual liquidity (what exists across systems)

4. Visible vs Hidden Liquidity

5. Real Trading Behavior

Traders are experiencing:

-

price jumping across levels instead of moving smoothly

-

entries executed at worse prices than expected

-

stop-loss clustering and rapid triggers

-

difficulty holding positions

6. How Liquidity Actually Breaks Down

Here’s what happens during a typical trade:

-

Trader places order

-

Algorithm detects activity

-

Liquidity providers adjust or pull orders

-

Price moves quickly

-

Order gets filled at worse price (slippage)

This creates a feedback loop:

trading activity → liquidity withdrawal → price instability

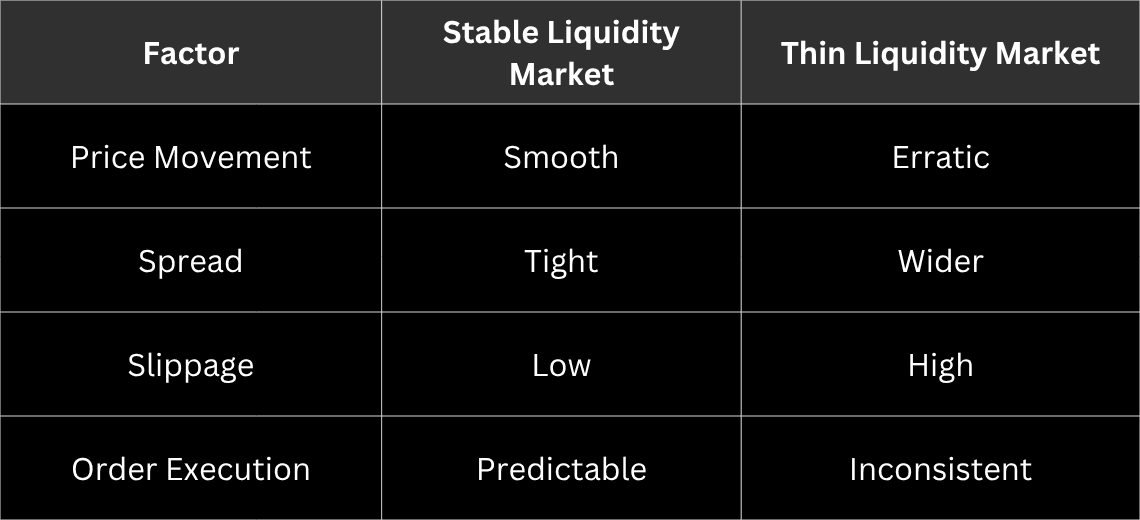

7. Stable vs Thin Liquidity Conditions

8. Strategy Breakdown in Thin Liquidity

Traditional strategies struggle because they assume:

-

stable execution

-

consistent spreads

-

predictable movement

In thin liquidity conditions:

-

breakouts fail

-

entries become less accurate

9. Big Code Block: Liquidity-Aware Strategy Concept

//@version=6

strategy("Liquidity Aware Volatility Strategy", overlay=true)

// Inputs

atrLen = input.int(14)

volThreshold = input.float(1.4)

// Indicators

atr = ta.atr(atrLen)

atrMA = ta.sma(atr, atrLen)

// Detect volatility expansion (proxy for thin liquidity)

thinLiquidity = atr > atrMA * volThreshold

// Range detection

highRange = ta.highest(high, 20)

lowRange = ta.lowest(low, 20)

// Avoid breakout trades in thin liquidity

longCondition = not thinLiquidity and close > highRange

shortCondition = not thinLiquidity and close highRange

// Entries

if (longCondition)

strategy.entry("Long", strategy.long)

if (shortCondition)

strategy.entry("Short", strategy.short)

if (meanLong)

strategy.entry("Mean Long", strategy.long)

if (meanShort)

strategy.entry("Mean Short", strategy.short)

// Risk management

strategy.exit("Exit Long", "Long", stop=close - atr, limit=close + atr * 2)

strategy.exit("Exit Short", "Short", stop=close + atr, limit=close - atr * 2)

10. Practical Insight for Traders

To handle thin liquidity conditions:

-

avoid trading during extreme volatility spikes

-

use wider stop-loss levels

-

reduce position size

-

focus on confirmation-based entries

-

avoid relying only on breakout strategies

11. Conclusion

Liquidity in U.S. markets hasn’t disappeared, it has changed form.

Markets have shifted from:

-

deep → fragmented

-

stable → reactive

-

predictable → execution-sensitive

That’s why traders now experience:

-

more slippage

-

faster price moves

-

less reliable setups

The key takeaway:

High volume does NOT guarantee high liquidity.

To stay consistent, traders need:

-

strategies that adapt to execution conditions

-

systems that account for volatility and liquidity shifts

-

faster iteration and testing workflows

Instead of manually building and debugging strategies in this complex environment,

PineGen AI helps you convert trading logic into structured Pine Script, test faster, and adapt to real market conditions without wasting time on code issues.