Payment for Order Flow at Record Highs: Is Retail Trading Distorting U.S. Market Structure?

Author : Ranga Technologies

Publish Date : 5 / 6 / 2026 • 3 mins read

Last Updated : 5 / 6 / 2026

Over the past decade, U.S. markets have gone through one of the biggest structural shifts in modern trading history.

Commission-free trading removed entry barriers. Mobile-first platforms brought millions of retail traders into equities and options. Trading activity surged across nearly every session.

On the surface, this looks like a democratized market. But underneath, a less visible mechanism plays a central role in how trades are executed:

1. Payment for Order Flow (PFOF)

PFOF is not just a brokerage revenue model. It is a routing system that determines where retail orders go, how they are executed, and how much of that flow is visible to the broader market.

And today, its scale is no longer marginal.

2. The Scale of PFOF in Modern U.S. Markets

Recent industry and Moody’s 2025–2026 market structure analysis shows how deeply embedded PFOF has become:

-

27% of total U.S. equity volume is linked to payment for order flow

-

51% of U.S. options volume is routed through PFOF structures

This means: More than half of options trading and over a quarter of stock trading now involves internalized execution flows rather than direct exchange interaction.

Even more important is where this flow goes:

-

~90%–95% of retail market orders are executed off-exchange

-

96% of equity PFOF flow is executed by market makers rather than lit exchanges

-

94% of options PFOF flow is also internalized by market makers

What this reveals is a structural reality:

Most retail trading activity no longer directly interacts with public exchange order books.

That single shift changes how price discovery works.

3. Why Payment for Order Flow Exists (And Why It Scales)

To understand PFOF, you have to understand incentives.

Retail orders are valuable because they are:

-

smaller in size

-

less informed

-

more statistically predictable

-

easier to hedge

Market makers are willing to pay for this flow because they can:

-

capture spread differences

-

hedge exposure efficiently

-

internalize execution profitably

-

manage inventory with controlled risk

At the same time:

-

brokers receive revenue from routing flow

-

traders receive commission-free execution

This creates a system where: execution routing becomes economically optimized rather than purely transparency-driven.

4. How Market Structure Changes Under PFOF

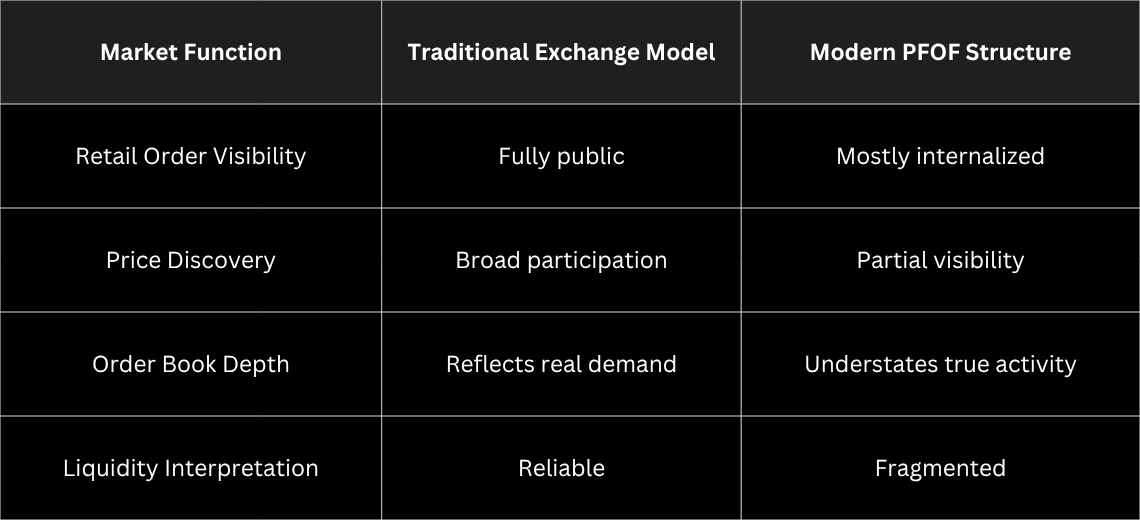

Traditionally, markets functioned through public order interaction:

-

Orders hit exchanges

-

Order books update in real time

-

Visible liquidity reflects demand and supply

-

Price discovery happens transparently

Under modern PFOF-heavy structure:

-

Retail orders are routed to wholesalers

-

Orders are executed internally

-

Exchanges never fully see that flow

-

Public price updates without complete participation data

This creates a key structural gap: Price becomes visible, but a significant portion of the flow shaping it does not.

5. Exchange vs Internalized Flow Reality

6. Why “High Volume” No Longer Guarantees Strong Liquidity

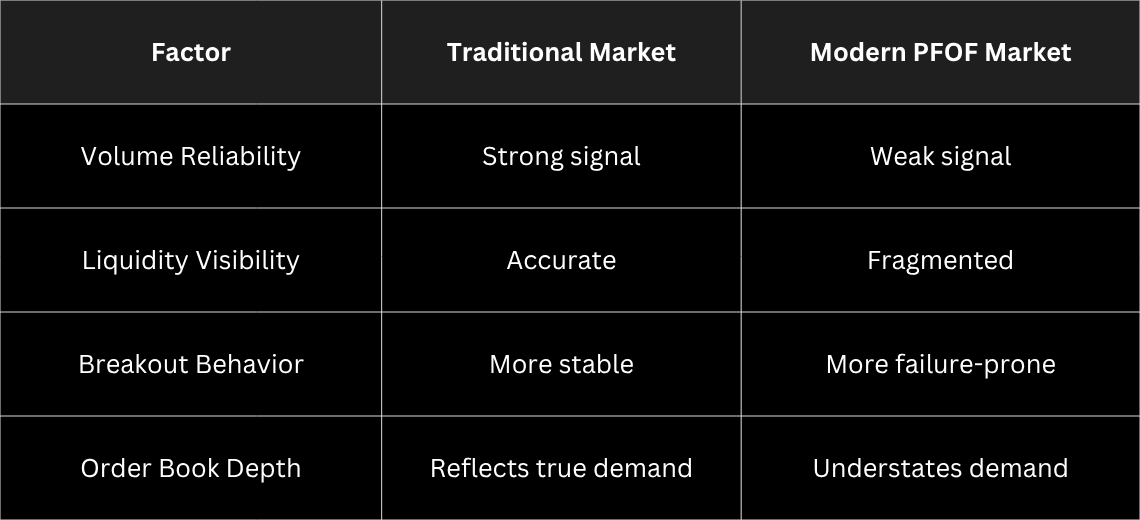

One of the most misunderstood aspects of modern markets is the relationship between volume and liquidity.

Historically:

- high volume = strong participation

- strong participation = reliable liquidity

That relationship is weaker today.

Even though markets show massive activity:

-

retail flow is largely internalized

-

exchange books only reflect partial participation

-

visible liquidity often underrepresents actual trading interest

This explains a common trader observation:

Markets feel thinner and more volatile even during high-volume sessions.

The reason is structural:

-

displayed liquidity is not the full liquidity

-

order books no longer capture complete demand

7. Why Breakouts Fail More Often in Modern Market Conditions

Breakout strategies depend on a simple idea:

When price breaks a level with volume, participation confirms direction.

But in fragmented execution environments:

-

visible volume may not represent full order flow

-

breakout pressure may be absorbed internally by market makers

-

hedging activity can counteract directional moves

As a result:

-

breakouts trigger but fail quickly

-

continuation lacks follow-through

-

wick-heavy reversals increase

This creates an environment where Price can move without fully transparent participation behind it.

8. The Role of Market Makers in Modern Price Formation

With a large share of retail flow internalized:

-

market makers become central liquidity intermediaries

-

they hedge exposure dynamically across venues

-

their risk management directly influences short-term price movement

For example:

-

heavy retail buying → market makers hedge short

-

heavy retail selling → market makers hedge long

These hedging flows create secondary market pressure that can:

- amplify volatility

- accelerate reversals

- distort short-term momentum

So price movement is no longer purely buyer vs seller.

It is increasingly:

Retail flow + intermediary hedging + fragmented execution behavior

9. Modern Market Conditions vs Traditional Assumptions

10. Why This Matters for Strategy Design

Most retail strategies still assume older market mechanics:

-

volume confirms direction

-

order book reflects liquidity

-

breakouts reflect real demand

-

price moves organically

But under modern structure:

-

volume is fragmented

-

liquidity is partially hidden

-

execution is internalized

-

price movement is influenced by hedging systems

This creates a mismatch between how strategies are designed vs how markets actually behave.

11. Strategic Adaptation in Modern Conditions

To adapt, modern trading systems increasingly require:

1. Volatility-Based Filtering

Instead of raw breakout entries, systems need volatility context (ATR, range compression, expansion states).

2. Confirmation Logic

Price alone is no longer enough; multiple conditions must align before entry.

3. Adaptive Risk Models

Position sizing must adjust based on regime changes.

4. False Breakout Protection

Retests and confirmation candles reduce noise-driven entries.

5. Multi-Factor Validation

Combining trend, volatility, and structure improves reliability.

12. Why PineGen AI Becomes Relevant Here

As market structure becomes more fragmented, strategy development becomes harder to do manually.

PineGen AI helps address this by enabling:

-

structured multi-condition strategy building

-

faster iteration across different logic versions

-

built-in debugging and explanation

-

rapid testing of alternative setups

-

scalable strategy refinement workflows

Instead of building strategies on simplified assumptions, traders can design systems that reflect modern market behavior, not outdated structural models.

13. Conclusion: A Market That Looks Simple, But Isn’t

Payment for Order Flow has expanded access to trading and reduced explicit costs for retail participants.

But it has also reshaped how markets function beneath the surface.

Today’s U.S. market structure is defined by:

-

high internalization of retail orders

-

fragmented liquidity visibility

-

reduced transparency in price discovery

-

increased influence of market maker hedging behavior

The result is a market that appears active and liquid…

but behaves more complexly than traditional models suggest

For traders, the key takeaway is simple:

Visible data is no longer the full data.

Strategies that ignore this structural shift risk underperforming in modern conditions.

Markets evolve continuously.

Execution models change.

Liquidity structure changes.

Price discovery changes.

Your strategy design process needs to evolve with it.

Use PineGen AI to build TradingView strategies designed for:

-

fragmented liquidity environments

-

modern execution structures

-

volatility-driven market regimes

-

adaptive strategy logic

Build strategies for how markets behave today, not how they used to behave.